Open your admin portal. Pull the tire and wheel claim report for the last 24 months.

Look at the claim ratio.

Now look at the quarter before that.

Chances are the trend is not going in the direction your underwriters would call healthy.

Tire and wheel has long been one of the most problematic F&I products in automotive retail. Not because the product is wrong — dealers sell it because customers genuinely need it. But because the claims math, over time, tends to move against the dealer. Claims frequency is high. Claim amounts are real. And the reserve accounting that sits behind a book of tire and wheel business can quietly absorb more dealer capital than anyone in the store fully realizes.

This is not an article about why tire and wheel is bad. It’s an article about why the economics are harder than they look — and what a new category of tire protection is starting to change about that picture.

The Claim Ratio Problem Nobody Talks About

In F&I product circles, a healthy target claim ratio for an ancillary product is generally considered to be below 60%. That means for every dollar collected in premium, fewer than 60 cents goes out in claims. The rest covers admin, profit, and reserve contribution.

Tire and wheel historically runs above that. In conversations with dealers across the country, claim ratios of 70%, 80%, even 120% or higher on specific terms are not unusual. When a book runs at 120%, the dealer is paying out more in claims than they’re collecting in premium — and that’s before admin fees, adjustments, and reserve holds.

Why is frequency so high?

Because flats are common. Road debris is everywhere. Potholes are a municipal budget problem that never gets fully solved. And when a customer gets a flat, they file a claim — that’s what the product is for. The claims aren’t fraud. They’re just… frequent.

The math works when the product is priced correctly, when the book is large enough to spread risk, and when the administrator manages claims tightly. But for the average single-point or small group dealer, the book may not be large enough to absorb the volatility. One bad quarter — a winter with unusual road salt damage, a construction season with elevated debris — and the reserve account takes a hit that doesn’t show up until the quarterly review.

What “Reserve Leakage” Actually Means

Most dealers understand reserve accounting in theory. Premium is collected. A portion is held in reserve. Claims are paid out of that reserve. At the end of the term, if the book performed well, money can come back.

What fewer dealers track in real time is the compounding effect of ongoing claim ratios above breakeven. When a book runs at 90–100% claim ratio consistently, the dealer isn’t losing money on every claim — they’re also not building the reserve cushion that makes the product profitable over time. The “profit” becomes theoretical, held hostage to one bad season of road conditions.

Worse: if the dealer is reinsuring their own book, they are directly exposed to that claim ratio. Every claim paid comes out of the dealer’s own reserve account. The tire and wheel product looks like an F&I win on the menu — and slowly becomes a reserve drag in the background.

The Used Vehicle Amplifier

The problem is worse on used vehicles. High-mileage units, off-lease cars, and trade-ins with 30,000+ miles already on the tires are the units where tire and wheel is most needed — and where the claim frequency is highest.

A 2019 Honda CR-V with 45,000 miles comes in on trade. The tires look decent. The customer wants tire and wheel. The F&I manager presents it, the customer buys, everyone feels good.

Eighteen months later, that customer has had three flats and two road hazard claims. The claim ratio on that specific vehicle has already exceeded the annual premium collected. The dealer is now drawing down reserves on a unit they retailed 18 months ago.

This is the specific problem that makes tire and wheel on used vehicles a different economic animal than on new. The risk profile isn’t known at point of sale. The tires may have invisible prior damage. The customer may be a high-mileage driver who never disclosed their driving patterns. And the claim shows up long after the deal is done.

Why Traditional Tire and Wheel Can’t Fully Solve This

Traditional tire and wheel products — the ones administered through a third-party administrator, backed by an insurance carrier, with a defined claim process — are well-structured products. The best ones (JM&A Tire and Wheel, EasyCare, Chubb, others) have sophisticated claims management, clear coverage terms, and strong provider networks.

But they are, fundamentally, indemnity products. They pay claims after something bad happens. They don’t prevent the event. They manage the cost of it.

And no matter how efficiently an administrator processes claims, the claims still happen. The customer still gets the flat. The dealer still processes the claim. The reserve still moves.

This is the structural limitation of every traditional tire and wheel product on the market. They’re all solving the same part of the problem — the reimbursement — without touching the event that creates the claim in the first place.

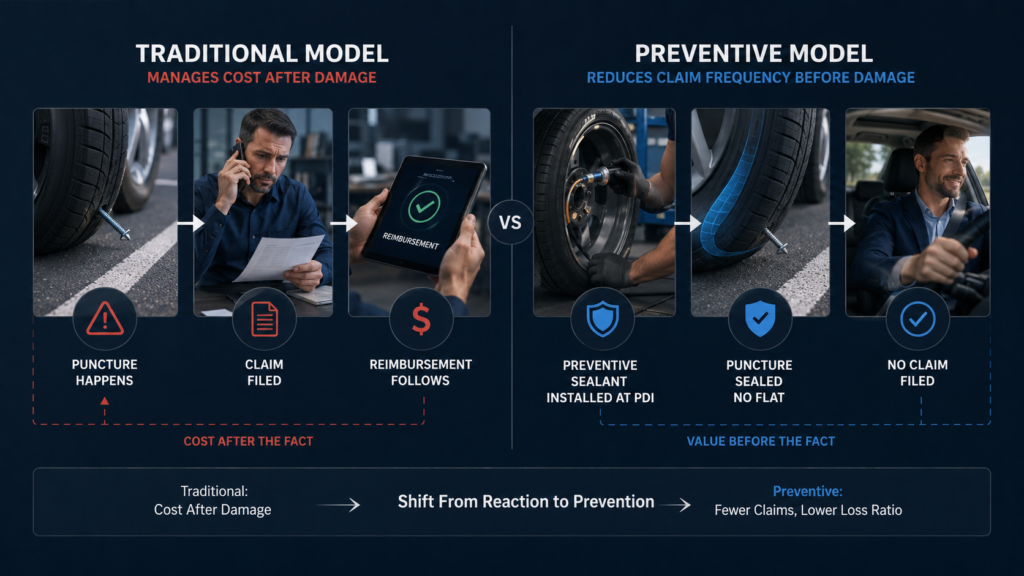

The Difference a Prevention Layer Makes

This is where a different category of tire product enters the picture. Protective tire sealant — installed at PDI, before the customer ever drives the vehicle — works differently. It prevents the puncture from becoming a claim.

The distinction matters for the economics:

- A traditional tire and wheel policy pays $150–$400 per claim. Over a 12–36 month term, that adds up.

- A preventive sealant may eliminate the need for that claim entirely. The flat doesn’t happen. The claim isn’t filed. The reserve isn’t touched.

This doesn’t mean preventive sealant replaces tire and wheel. It means it changes the claim profile of the vehicles it’s installed on. Fewer claims filed against a tire and wheel book means a better claim ratio — which means better reserve performance — which means more money staying in the dealer’s account.

Dealers who have layered a preventive sealant into their F&I workflow are starting to report this effect: the vehicles with sealant installed show a different claims pattern than the vehicles without it. Not because the book was cherry-picked — but because the sealant changed the underlying risk on those units.

What This Means for Your F&I Strategy

If you’re running a tire and wheel book, you’re not just managing a product. You’re managing a reserve exposure that accumulates over the life of every vehicle you’ve sold with the product.

The dealers who are winning on tire and wheel right now are the ones who have found a way to reduce claim frequency without reducing the value of the coverage. Preventive tire sealant is one tool in that direction.

The conversation to have with your F&I director, your administrator, and your service team is simple: what would our claim ratio look like if 20% of our tire and wheel vehicles never had a flat? What would our reserve account look like if that continued for 36 months?

That’s the math worth running.