Show me an F&I product that works after the flat happens.

That’s the starting point for just about every tire and wheel product in automotive retail. Road hazard coverage, tire and wheel protection, cosmetic wheel protection — they share the same basic structure. Something bad happens to the customer’s tire. The customer files a claim. The administrator reviews it and pays out. Everyone moves on.

This is good business. It solves a real problem. Customers value it, dealers profit from it, and administrators manage it efficiently. The model works.

But it’s also a reactive model. Every dollar that flows through it flows because something went wrong first.

Now think about what happens if you could change the event itself — not just manage the cost after it happens.

What “Prevention” Means in an F&I Context

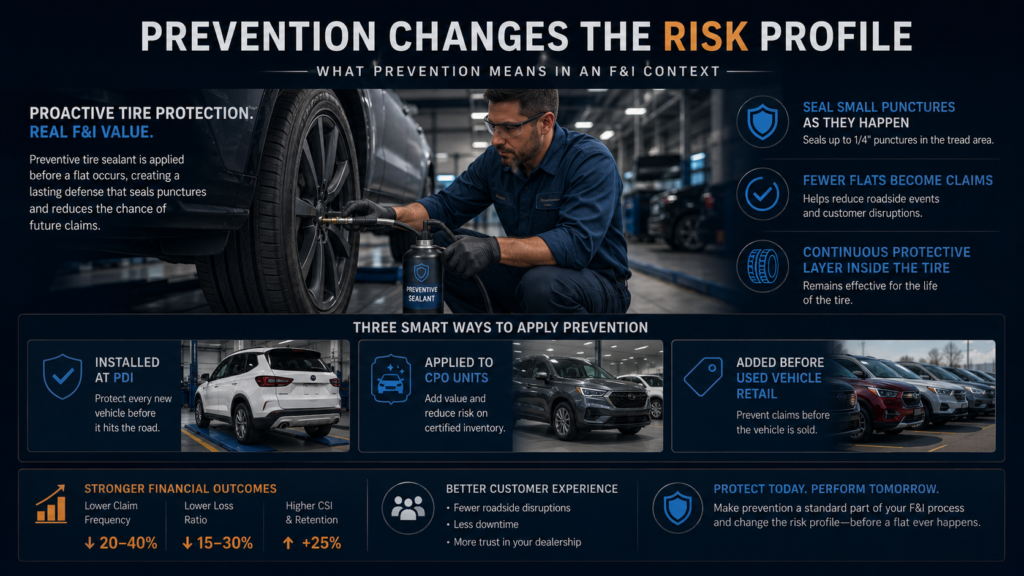

In the context of F&I products, “prevention” doesn’t mean the customer never gets a flat. It means fewer flats occur, fewer claims get filed, and fewer dollars flow out of the reserve account.

The product that does this is a preventive tire sealant — applied to the inside of the tire through the valve stem, bonding with the rubber, sealing small punctures as they happen, usually without the customer ever noticing.

Installed at PDI on a new vehicle. Installed on a CPO unit before it goes to the lot. Applied to a used car before it retails. In each case, the product changes the risk profile of the tire on that vehicle — not by changing the tire, but by adding a continuous protective layer that prevents the most common puncture scenarios from creating a claim.

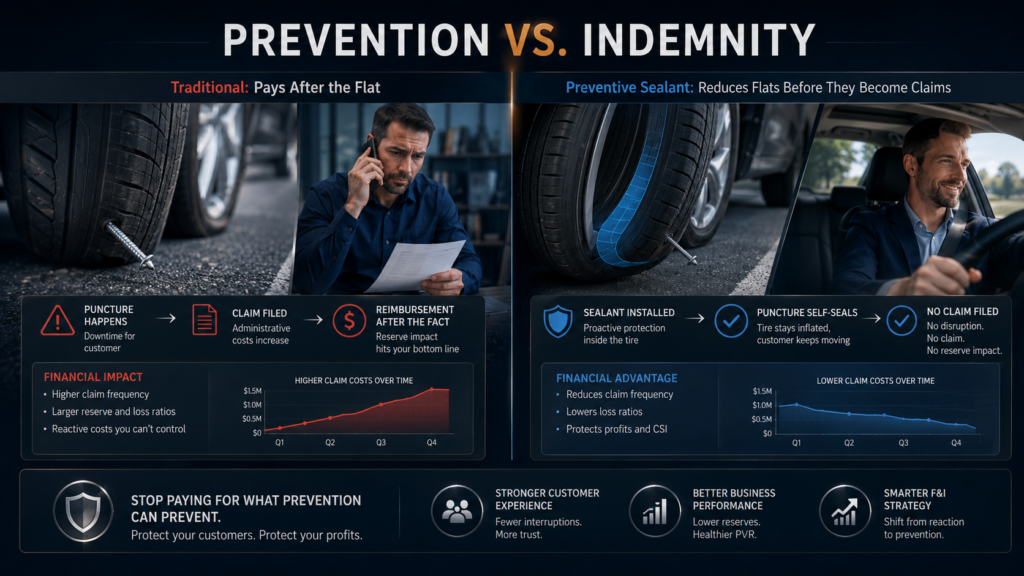

The Core Distinction: Prevention vs. Indemnity

This is the distinction that matters for how you position it, present it, and sell it:

Indemnity products (traditional tire and wheel): Pay the customer money after a covered event occurs. The customer gets a flat. The customer pays out of pocket or gets reimbursed. The claim is processed. The reserve account moves.

Preventive products (sealant): Reduce the probability and frequency of covered events. The customer gets a nail. The nail is sealed. The customer never calls the administrator. The claim is never filed. The reserve is never touched.

The customer experience under indemnity is: something bad happened, and I was made whole.

The customer experience under prevention is: something bad almost happened, and I didn’t even know it.

Neither is better in the abstract. But for the dealer’s reserve account, the math is meaningfully different. Prevention reduces claim frequency. Reduced claim frequency improves claim ratios. Improved claim ratios mean more money stays in the reserve account — money that, in a reinsured structure, flows back to the dealer.

Why F&I Managers Are Paying Attention to This

The F&I managers who are looking at preventive tire sealant are not replacing their tire and wheel program. They’re asking a more specific question: what is the claim ratio on the vehicles that have this product versus the ones that don’t?

If the sealant is reducing the number of flats on those specific vehicles, the claim ratio on the sealant-protected portion of the book should be measurably different from the rest of the book. That delta is where the value lives.

A dealer with a 90% claim ratio on tire and wheel is essentially breaking even on the product — collecting enough premium to pay out roughly that much in claims, with minimal contribution to overhead or profit beyond the admin fee. If preventive sealant reduces that claim ratio by 20–30 percentage points on the vehicles where it’s installed, the product is contributing real economic value to the F&I office that doesn’t show up on the menu.

This is why the pilot program structure matters. Start with 20 vehicles. Track the claim experience on those 20 vehicles against the rest of the book. Run the numbers for 12 months. If the sealant-protected vehicles are showing a meaningfully different claim frequency, you have real data to bring to your administrator, your lender, and your dealer principal.

How to Position It to the Customer

The customer conversation is actually simpler than the economics.

Every customer who buys a car fears the flat tire. They fear it because it’s inconvenient, because it costs money they didn’t budget for, and because it tends to happen at the worst possible time. They fear it more than they fear engine failure or transmission trouble — because it’s happened to them before, and the other stuff mostly hasn’t.

The traditional tire and wheel pitch addresses that fear by offering to pay for it if it happens. “If you get a flat, you’re covered.”

The preventive sealant pitch addresses that fear differently: “Most flats, we can prevent from happening at all.”

For the customer, this is a better story. Not just “you’ll be reimbursed” — “you probably won’t need to be.” Nobody wants to use their road hazard coverage. Everyone prefers to not need it.

The F&I manager who can lead with that — who can show the customer a tire that’s been punctured and sealed, right there in the office — has a demo that no other F&I product can match. The product sells itself when the customer can see it working.

How to Position It in the Menu

The menu structure is where most F&I managers will make their decision about how to present this product.

Two clean options:

Standalone: Positioned as the tire protection product on the menu. 12-month coverage, $124 per vehicle (pending confirmed pricing). The customer gets puncture sealing, pressure maintenance, and peace of mind. Simple story, simple math for the customer.

Integrated with tire and wheel: Present the 12-month included sealant as the foundation of the tire and wheel menu, with an upgrade path to 3, 5, or 7-year tire and wheel coverage. “The 12-month protection is included with your vehicle — and if you want to continue that coverage for the full term of ownership, here are your options.” This reframes the conversation from “do you want to add something?” to “how would you like to continue what you already have?”

Either structure works. The key is not burying it in the terms. The key is making the prevention story central — because that’s the thing that makes this product different from every other tire product on your menu.

The Claim Prevention Pitch Is Not a Promise

It’s important to be clear about what preventive sealant does and doesn’t do. It seals punctures up to 1/4 inch in the tread and crown area. It does not seal all punctures, all the time, regardless of size or conditions. It’s not a magic shield.

But it doesn’t need to be. The goal is to shift the claim ratio on the vehicles it’s installed on — not to eliminate every possible flat. If it reduces the number of claims filed by 30%, the economics of the F&I book improve meaningfully. If it reduces them by 50%, the improvement is significant.

The pitch is honest: “This product prevents most of the flats that would otherwise turn into claims. Not all of them — but most of them. And that changes what happens to your service department, your reserve account, and your customer satisfaction scores.”

F&I managers who understand this are the ones who will use it well.